Feeling weighed down by debt while trying to save for retirement? You’re not alone. Many Canadians are juggling mortgages, lines of credit, and family expenses while still hoping to retire comfortably.

The numbers tell the story. According to Statistics Canada, the household credit market debt-to-disposable income ratio reached 173.9% in Q1 2025—the second-highest level on record. That means Canadians owe about $1.74 for every dollar they take home. Even though debt servicing costs are stable at around 14.4% of disposable income, the sheer size of household debt can feel overwhelming.

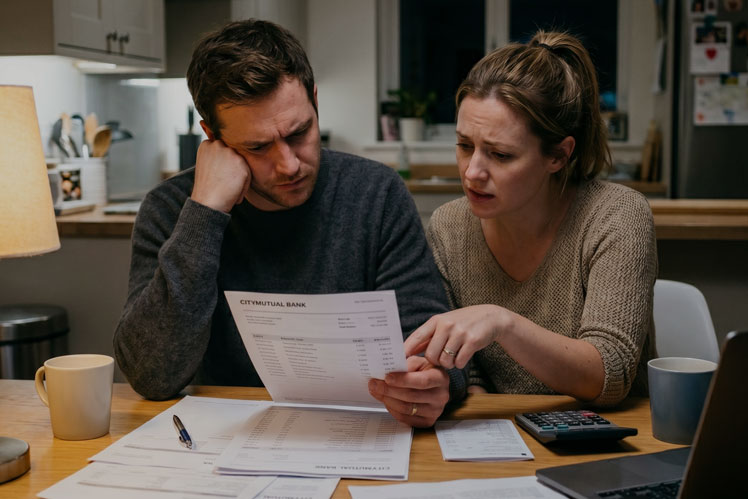

Meet Sam and Marsha

Sam and Marsha, both in their mid-40s, have a 17-year-old daughter, Alicia, who’s gearing up for college. They’ve always been careful with money compared to many of their peers, but retirement planning hasn’t been their main focus.

Up until now, their priority has been ensuring Alicia gets a solid education. They’ve steadily contributed to her Registered Education Savings Plan (RESP) and have $12,500 set aside for her schooling. Their own savings total $11,000—not much considering retirement is inching closer.

Financially, here’s where they stand:

- Income: About $150,000/year between Sam’s contracting work and Marsha’s teaching salary.

- Assets: Two properties— their family home and a small rental—both of which have maintained value.

- Debt: $564,000 in mortgages and an $18,000 home equity line of credit.

- Net Worth: Roughly $205,000.

Marsha will eventually have a solid pension, and the rental could generate an extra $1,000/month once it’s mortgage-free. But until Alicia finishes college, retirement contributions will be minimal.

The Plan to Get Back on Track

- Tackle the Debt First

While Alicia is in school, their best move is to aggressively reduce debt—especially their line of credit—and avoid new borrowing. The less interest they pay, the more they’ll have for retirement later. - Accelerate Mortgage Payments

Switching from monthly to weekly payments or adding lump-sum principal payments can shave years off a mortgage. This strategy acts as a “forced savings plan” by building home equity faster. - Redirect Education Funds Post-Graduation

Once Alicia’s education expenses end, the money currently going toward tuition can be redirected into retirement savings and additional mortgage payments. - Hold on to the Rental Property

Selling the rental might seem like a quick way to reduce debt, but keeping it could provide valuable retirement income once the mortgage is gone.

Why It’s Worth It

With debt levels in Canada at near-record highs, a strategic approach is essential. Paying down debt now reduces stress, increases flexibility, and sets the stage for a stronger retirement. Sam and Marsha’s situation is a reminder that it’s never too late to create a clear financial roadmap.

By combining steady debt repayment with disciplined saving, they can move toward financial independence—one payment at a time—and step into retirement with more freedom and less worry.

Contact our office to learn more about how a wise debt management plan can open more retirement possibilities.

Need help with your retirement strategy?

Contact our office

Copyright © 2025 AdvisorNet Communications. All rights reserved. For informational purposes only and is based on the perspectives and opinions of the owners and writers only. The information provided is not intended to provide specific financial advice. Readers are advised to seek professional advice before making any financial decision based on any of the ideas presented in this article. This copyrighted information presented online is not to be copied, or clipped or republished for any reason. The publisher does not guarantee the accuracy and will not be held liable in any way for any error, or omission, or any financial decision.