Scott Havens* is the kind of guy everyone wishes they had in their life. At 35, he’s the go-to mechanic in Vancouver who never hesitates to lend a hand—whether it’s helping a buddy fix a transmission or pulling over to help a stranger with a stalled engine. He’s the definition of dependable.

But nothing prepared Scott for what happened when his mom, Anne, needed him in a whole new way.

Anne, who lives in a downtown Vancouver high-rise, was recently told her Parkinson’s disease was progressing faster than anyone expected. She had to stop working. Scott, without blinking, moved in to help. Now, he balances caregiving with work—only able to clock in when a kind neighbor takes over for a few hours. And with Anne’s medical needs growing by the week, the cost of care and medication shows no sign of slowing down.

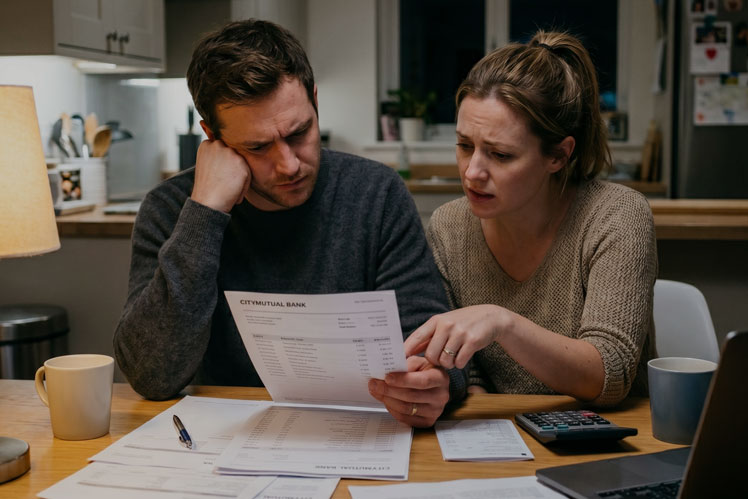

Scott’s story isn’t unique. More and more adult children are finding themselves in this unexpected caregiver role. One moment they’re planning for their kids’ future—saving for college or a home upgrade—and the next, they’re trying to figure out how to support aging parents, physically, emotionally, and financially.

Professional eldercare, especially in a full-time facility, can cost as much as a year of university tuition—per month. It’s no wonder many families decide to provide care themselves. But that often means someone cuts back hours at work—or leaves the workforce altogether. Schedules shift. Family routines change. And sometimes, so do financial goals. Add in the fact that many elders live with chronic conditions for years, and the pressure keeps building.

But there’s another side to this story. On the other side of town, Bruce Metcalf* and his wife Suzie had a different experience with Bruce’s dad, Tom. A few years ago, when Tom was still healthy and independent, Bruce sat down with a financial advisor and had a serious conversation about the future.

As an only child, Bruce knew the responsibility would fall on him if something ever happened to his dad. So, he convinced Tom to apply for long-term care insurance while he was still eligible. It felt like a “just-in-case” move at the time—but today, it’s become a lifeline.

Recently, Tom’s vision deteriorated due to macular degeneration. He could no longer work or even navigate safely on his own. That long-term care policy? It kicked in and is now covering the costs of the support Tom needs.

For Bruce, it’s a massive relief. He can be present for his dad without upending his entire life or draining his family’s savings.

The bottom line? Eldercare isn’t something we think about until it’s staring us in the face—but by then, it can be overwhelming. Having a plan—whether it’s a conversation, a strategy, or the right insurance—can make all the difference between struggling through and being able to care with confidence.

*Fictional characters for illustrative purposes only.

Dealing with Eldercare realities starts with a plan.

Contact our office

Copyright © 2025 AdvisorNet Communications. All rights reserved. For informational purposes only and is based on the perspectives and opinions of the owners and writers only. The information provided is not intended to provide specific financial advice. Readers are advised to seek professional advice before making any financial decision based on any of the ideas presented in this article. This copyrighted information presented online is not to be copied, or clipped or republished for any reason. The publisher does not guarantee the accuracy and will not be held liable in any way for any error, or omission, or any financial decision.